Did you know that 7 out of 10 South African adults pass away without a valid Will? This leaves families vulnerable, delays estate processes, and risks losing cherished legacies.

Wills Month—an initiative led nationally by the Law Society of South Africa—aims to change this. At Aquilla Financial Solutions, we proudly stand with this mission to make estate planning accessible, compassionate, and deeply personal.

Why a Will Matters

A Will is much more than just paperwork or a legal formality. It’s a powerful way to protect the people and things you care about most. Think of it as a heartfelt safeguard that makes sure your loved ones are taken care of exactly as you wish, easing their burden during difficult times.

Beyond the practical details, a Will is also a reflection of who you are — your values, hopes, and the legacy you want to leave behind. It gives you the chance to clearly express your final wishes, helping to prevent confusion, disagreements, or misunderstandings among family members when you’re no longer here to guide them.

Ultimately, creating a Will is an act of love and responsibility. It’s a way to ensure that your story, your achievements, and your care continue to live on in the way you intend.

To summarize, a will is:

- A safeguard to protect your loved ones

- An expression of your values and final wishes

- A tool that prevents conflict and confusion

- A way to ensure your legacy endures

Our Commitment: “You Refer, We Fulfil”

This September, we’re teaming up with Capital Legacy for their “You Refer, We Fulfil” initiative. Here’s how it works:

- Refer someone who needs a Will

- We assist them in drafting it—professionally, compassionately, and free of charge

- We securely store the signed Will in safe custody

- Whether or not they opt for the premium plan to cover estate costs, their legacy remains protected

Our simple goal this Wills Month is to make a difference in just one life. Because one Will can ease the heartache of loss. One conversation can transform a family’s future. One referral can safeguard a legacy.

Your Legacy, Your Way

At Aquilla Financial Solutions, we believe estate planning should be rooted in empathy, clarity, and care. Let’s make September meaningful—one Will, one life, one legacy at a time.

If you or someone you know would benefit from this initiative or have questions, please don’t hesitate to reach out.

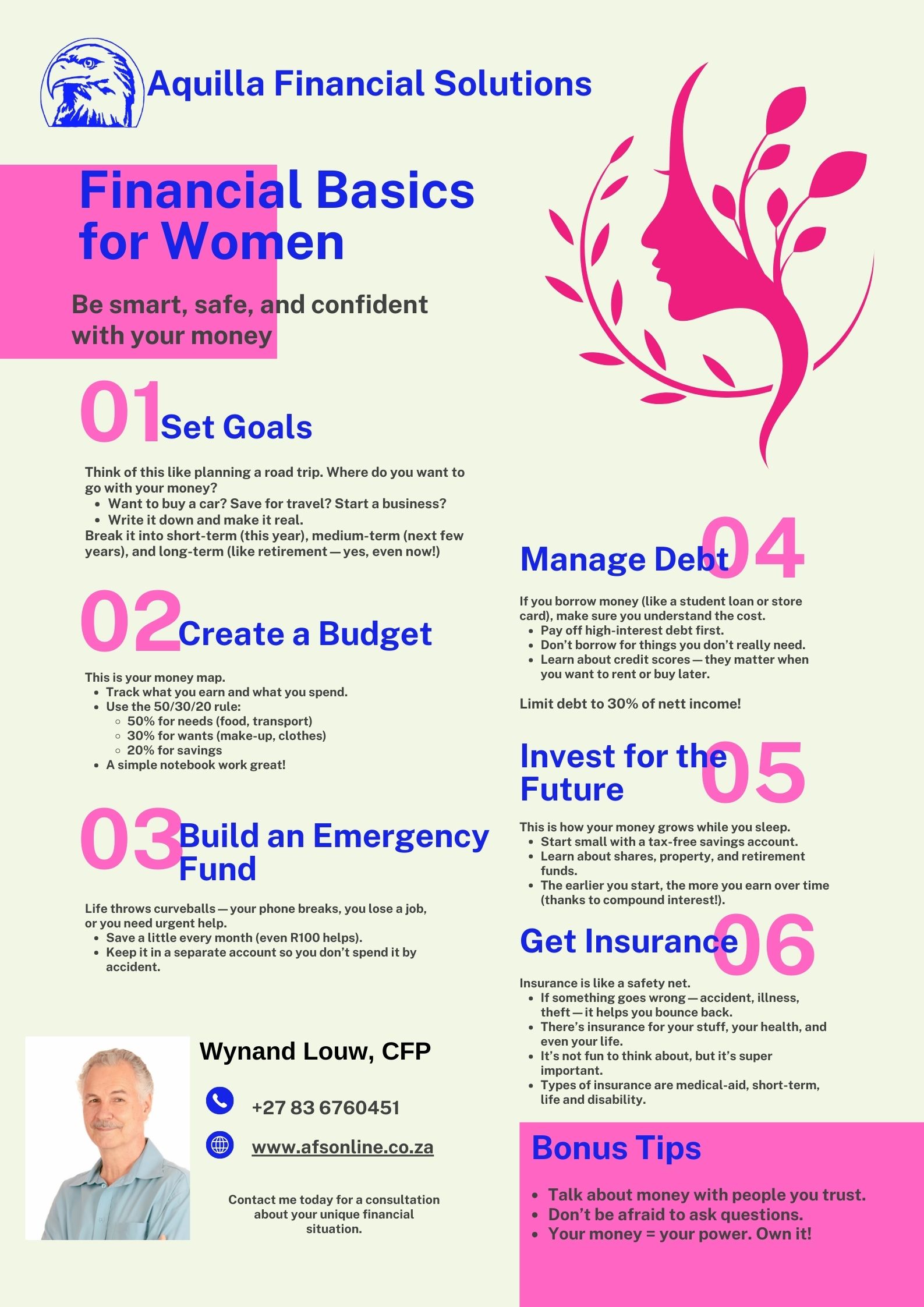

As we celebrate Women’s Month, it’s important to reflect not only on the social and cultural achievements of women but also on financial empowerment. Money management is a vital skill that every woman deserves to master. Whether you’re just starting your financial journey or looking to sharpen your skills, understanding the basics can open the door to greater independence, security, and confidence.

At Aquilla Financial Solutions, we believe that financial literacy is a key step toward owning your future. That’s why we’ve created this easy-to-follow guide designed specifically for women, to help you be smart, safe, and confident with your money.

1. Set Clear Goals

Think of your money like a road trip. What’s your destination? Are you saving for your first car, a dream vacation, or perhaps starting your own business? Writing down your goals and categorizing them into short-term (this year), medium-term (next few years), and long-term (like retirement) is crucial. This exercise helps you visualize your financial road map, keep focused, and make your aspirations real.

2. Manage Debt Wisely

Not all debt is bad, but it’s essential to understand the true cost before borrowing. Always prioritize paying off high-interest debt like credit cards or store accounts first. Keep your debt limit within 30% of your net income to avoid financial strain. Learning about credit scores and how they impact your ability to rent or buy in the future is equally valuable.

3. Create a Budget That Works

A budget is your financial blueprint. We recommend the 50/30/20 rule—50% of your income goes to needs like food and transport, 30% to wants such as personal care or entertainment, and 20% to savings. Whether you use an app or a simple notebook, tracking your income and expenses will increase your spending awareness and control.

4. Start Investing Early for the Future

The power of compound interest means the earlier you start investing, the more your money can grow. Begin small with tax-free savings accounts and then explore shares, property, or retirement funds. Investing isn’t just for the wealthy—it’s a smart way to build wealth over time.

5. Build an Emergency Fund

Life is unpredictable, and having a financial safety net can give you peace of mind. Save a little each month—even R100 can add up over time—and keep this emergency fund separate to avoid dipping into it for daily expenses.

6. Protect Yourself with Insurance

Insurance can seem daunting, but it’s a vital safety net. Whether it’s medical aid, short-term insurance for your belongings, life insurance, or disability cover, having the right policies helps you recover from unexpected setbacks without compromising your financial security.

Your Money, Your Power

Money isn’t just about numbers. It’s about freedom, peace of mind, and opportunity. If you have questions or need personalized guidance, don’t hesitate to reach out. Wynand Louw, CFP, is here to help women build solid financial futures.

Celebrate Women’s Month by taking control of your money. Start today, and watch your confidence and wealth grow with every step.

It is that time of the year again when medical schemes are announcing their 2025 benefits and new contribution rates. So why are these medical schemes cost keep on rising way above the average inflation rate of South Africa? We have seen to date that contributions increased between 7.4% and even as high as 12.75% on more expensive plans on the schemes that have already announced their new contributions.

Healthcare costs are rising globally, and South Africa is no exception. Medical scheme members are often confronted with annual increases in contributions that outpace inflation, leaving many wondering why this happens. Several factors contribute to these hikes and understanding them can help you as a member to manage your healthcare budgets more effectively.

1. Medical Inflation vs. General Inflation

One key reason for the steep increases is the difference between medical inflation and general inflation. While general inflation reflects the rising costs of goods and services in the economy, medical inflation is often higher due to the increasing costs of medical technology, pharmaceuticals, and healthcare services.

New treatments and advanced diagnostic techniques, while improving health outcomes, come at a cost. As medical schemes need to cover these advancements, they pass the expenses on to their members.

2. Ageing Population

As South Africa’s population ages, medical schemes are seeing a larger portion of their membership base requiring more medical care. Older members tend to claim more frequently and for more expensive procedures and treatments, such as surgeries, chronic disease management, and long-term medications.

To balance out the rising claims from older members, medical schemes must increase contributions across the board to maintain financial sustainability.

3. Increased Disease Burden

The increasing prevalence of chronic diseases, such as diabetes, cancers, heart disease, and hypertension, places additional strain on medical schemes. Treating and managing these conditions over the long term is costly, leading to higher claims by members. With a higher disease burden, schemes need to adjust contributions to ensure they can cover these ongoing medical expenses for longer periods.

4. Medical Fraud and Over-Servicing

Another significant factor driving up costs is fraudulent claims and over-servicing.

Some healthcare providers or members may abuse the system by submitting false claims, while others may prescribe unnecessary treatments or procedures to increase billings. This misuse inflates the overall costs borne by the scheme, which is then recouped by raising member contributions.

5. Escalating Hospital and Specialist Fees

Private hospitals and specialists are key contributors to the increasing costs of medical schemes. Hospitalisation and specialist consultations are expensive, and the fees for these services continue to rise each year. As more members access private healthcare, schemes have to increase contributions to cover the rising fees.

6. Administration and Reserve Requirements

Medical schemes are also required by law to hold reserves equivalent to a certain percentage of their contributions. This ensures that schemes can cover unexpectedly high claims and remain financially stable. Maintaining these reserves, along with the cost of administering the schemes, adds to the financial burden and is another factor behind the contribution hikes.

7. Advances in Medical Technology

Innovations in medical technology, such as new diagnostic tools, surgical techniques, and advanced drugs, improve patient care but come at a higher cost. Medical schemes have to adjust their contributions to cover these cutting-edge treatments, ensuring that members have access to the best possible care.

What Can Members Do?

While contribution hikes may feel burdensome, there are ways for members to mitigate the impact:

- Review your plan annually to ensure it matches your healthcare needs. Also consider a free comparison with what other schemes might offer in comparison with your current scheme.

- Use the preventive care available on most schemes to reduce the need for expensive treatments later.

- Stay informed about changes in your scheme’s benefits and what options are available to manage out-of-pocket expenses.

Take control of your health and finances by ensuring your medical scheme is aligned with your needs. With 2025 medical scheme contribution increases ranging from 7.4% to 12.75%, it's essential to:

· review your options,

· update your plan if necessary, and

· make the most of your benefits.

Don't wait until the changes impact your budget; reach out to me today as your trusted advisor with 40 years of experience to explore your options and ensure you're getting the best coverage at the most affordable rate. I will provide you with a no-obligation comparison upon request.

In South African law, an engagement is considered a contract and breaking it off can have legal consequences. If a party breaks the engagement without lawful reason (unlawful termination), they may face claims for damages.

An engagement can be lawfully terminated without consequences under certain conditions, such as:

· mutual agreement,

· death of a party, or

· lawful repudiation for just cause

o (e.g., misrepresentation

o or wrongful conduct).

However, “unlawful termination” — ending the engagement without just cause, can lead to claims for both contractual damages and satisfaction under delict law.

Contractual damages include:

· Real damages: Expenses incurred in preparation for the marriage.

· Prospective loss: Compensation based on what the wronged party would have received if the marriage had occurred, though this is speculative and controversial.

Recent court cases

Recent court cases like “Van Jaarsveld v Bridges” and “Cloete v Maritz” have questioned the validity of claims for prospective loss, with the courts suggesting that engagement claims should not exceed the consequences of divorce. The idea that an engagement is more of a time to decide about marriage, rather than a binding contract, is gaining ground.

In conclusion

While claims for prospective loss are still debated, it’s becoming less likely that South African courts will allow such claims in the future based on Constitutional Grounds and outdated legislation within the new South African Society.

Consult and contact me to advise you on your financial options and possible consequences before you decide to get engaged or get married in conjunction with your attorney.

The short answer is yes, you can. However, certain conditions must be met for the new will to be valid. A recent case, “Roux N.O and Another v Stemmet N.O and Others”, highlights some of these key considerations.

In this case, the Western Cape High Court examined whether a person intended to revoke their existing will. The deceased, hospitalized with COVID-19, expressed a desire to revoke their will and create a new one. However, the court found that the necessary intent to revoke was absent, stressing the importance of complying with the requirements of the Wills Act. For more detail, see “Roux N.O and Another v Stemmet N.O and Others.” (17064/2022) [2023] ZAWCHC 222.

The Legal Framework

Section 2A of the Wills Act allows a court to declare a will revoked if the testator, in this case, the deceased: “drafted another document or before his death caused such a document to be drafted, by which he intended to revoke his will or part of his will and the court shall declare the will or the part concerned, as the case may be, to be revoked.” (Wills Act, 7 of 1953).

In this case, the court determined that the deceased did not personally draft the document upon which the trustees relied to revoke the 2018 will. Instead, it was drafted by the attorney, based on instructions from Mr. Willemse, not the deceased.

Additionally, the court found that the deceased never physically received, reviewed, approved, or signed the draft will in the presence of witnesses, as required by Section 2(1)(a) of the Wills Act. At the time the draft will was delivered by nursing staff, the deceased was in a coma, unaware of the document’s content and unable to confirm whether it accurately reflected his intentions.

As a result, the court concluded that the necessary “animus revocandi”—the intent to revoke—was absent.

Key Takeaways

Courts are generally cautious about declaring documents that do not meet the Wills Act’s requirements as valid wills. It is always advisable to seek assistance from an attorney or fiduciary expert when drafting or amending your last will and testament, especially as your circumstances or wishes change.

Update Your Will Regularly

It's essential to revise both your financial plan and will regularly. Any significant life event, such as the birth of a child, marriage, divorce, or the death of a family member, should prompt you to update your will.

For example, consider the case of Mr. X, who divorced his wife but never updated his will. He later remarried and had two children with his new wife. When Mr. X died 17 years after his divorce, his will had not been changed. This meant that his new wife and children could not inherit anything, as the original will, made before the divorce, remained valid.

Don’t Delay

Ensure your will is up to date and reflects your current wishes regarding your estate. Contact me today to avoid any potential issues or delays in obtaining your free will.

Latest News

- Wisdom Dental Insurance

- FAQs Demystifying Money Matters

- About Us

- Medical Schemes Open Season 2026: Making the Right Choice for You

- Single and Secure: Estate Planning That Honours Your Story

- Listening First, Planning Always: Tailored Wills for Every Single Parent’s Journey

- Wills Week 2025

- September is Wills Month — Protect Your Legacy with Compassion and Care

- Empowering Women This Women’s Month: Take Charge of Your Financial Future

- Why Medical Scheme Contributions Are Increasing

- Consequences if I want to break off my engagement

- Can I revoke my Last Will and Testament?

- Navigating the Impacts of the New Companies Act Amendments 2024

- Protecting your Digital Assets

- Important Changes to Non-profit Organisations (NPO) Act

- Working from home? What a scary thought!

- CIPC Compliance Checklist

- Where to from here?

- Unclaimed Retirement Benefits

- The Maze of Doing Business: Wantrepreneur or Entrepreneur?